How to Open a Bank Account Overseas

International bank accounts can be useful if you regularly transfer funds overseas or have assets in a foreign country. They can also be useful for business owners looking to diversify overseas.

In this article, we explore international bank accounts, how to open them, and some of the tax laws that apply to business conducted overseas.

What is an international bank account?

An international bank account, also known as an offshore bank account, is a bank account held outside your country of residence. International bank accounts are useful for accessing foreign currency whenever you need it, and providing a destination for your overseas transfers.

As well as the same day-to-day services as a domestic bank account, an international bank account allows you to hold, manage, and make payments using multiple currencies.

Pros

Cons

What can I do with an international bank account?

An international bank account makes it possible to hold money in another country, as well as making it easier to manage and transact in multiple currencies. Some banks also offer financial expertise and investment advice with an international account.

Most international bank accounts also provide the same services as domestic accounts, in that you can deposit and withdraw money, access a debit card, and manage your account as normal. There are sometimes limits on deposits and withdrawals which will be set by your chosen provider, so it’s important to read the terms and conditions of the account before you open it.

Why do I need an international bank account?

International bank accounts might be useful if one or more of the following scenarios apply to you:

You frequently pay or receive money internationally

If you often transfer money abroad, an international bank account will allow you to deposit it overseas, and also give you access to various currencies. Sometimes, you’ll be able to use multiple currencies in one international account, so all the currency you send or receive internationally can be deposited in one place.

You own assets abroad

If you own assets abroad, you may need a location to be able to deposit any profits, or a secure location if you wish to liquidate any assets. If this is the case, it’s a good idea to check the tax rules that will apply to you in both your domestic and host country before going ahead.

You provide financial support to friends and family abroad

An international bank account can be useful if you frequently provide financial support to friends and family, as you can have one central account through which you can manage all the funds you send overseas.

How to open an international bank account

All providers of international banking services will have slightly different requirements, but we’ve provided the steps below as a general guide.

Research the providers available

Contact your chosen provider and supply them with the required personal information

Provide any additional information as requested

Choose the currency you would like to hold

Make your first deposit

What are the requirements in my chosen destination?

Each country has its own rules and regulations when it comes to opening a bank account. We’ve listed some of the most popular destinations below.

Country | Requirements for opening an account |

|---|---|

Canada | ID verifying name and date of birth; Proof of address; Recent bank account or credit card statements; Passport |

France | Proof of residence; University letter (if enrolled)Letter from your previous bank (in some cases) |

Germany | Two forms of ID; Proof of registration if enrolled in school |

Italy | Passport; Valid visa; Proof of local address; Fiscal code (can be requested from a tax office or the Italian embassy |

Mexico | Form of ID; Proof of residence; Immigrant or non-immigrant visa |

The Philippines | Passport or other photo ID; Proof of address: Immigration documentation Accounts available are limited if you’ve been a resident for less than 180 days. |

Spain | Passport: Foreign ID number and certificate: Proof of local residence: University letter (if enrolled) |

The United Kingdom | Passport: Valid visa; Proof of local residence and residence in your home country; University letter (if enrolled) |

In some cases, you may be able to open an international bank account without needing to provide proof of address. However, under the Bank Secrecy Act, if you are a US citizen opening an international bank account, you must declare this when you apply. This is so the institution you’re banking with can make all the necessary declarations to the US government.

Revolut offers an international bank account and does not require you to provide proof of address. Find out more about Revolut.

How to deposit money into an international bank account

You can transfer money to your overseas bank account in a variety of ways, including:

A specialist international money transfer provider

A payment app

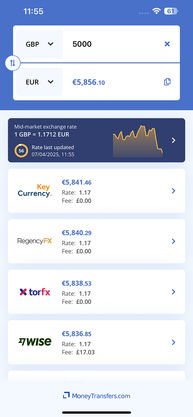

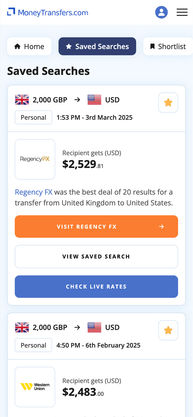

Often the cheapest, quickest way to transfer money overseas is with a specialist money transfer provider. In some cases your transfer will be free, and the exchange rates offered are usually cheaper than those offered by high street banks.

In contrast, wire transfers take a long time to process, and international wire transfers can be considerably more expensive. Likewise, some payment apps like PayPal also charge high conversion fees, and other apps like Zelle won’t be able to process transfers outside the US.

When you’ve opened your international account with an initial deposit, depositing further funds into the account is usually very similar to how you would deposit into your domestic account. Remember to keep an eye on your tax liability though, particularly if you’re earning money in a foreign country.

How to withdraw money from an international bank account

Withdrawing money from your international bank account is very similar to withdrawing from your domestic account, but there are some important things you’ll need to consider.

The exchange rate

The minimum account balance

Tax laws

How long does it take to open an international bank account?

It depends on your provider, but due to the level of checks needed to set up and verify your account, it can take anything between one and six months. To keep things moving as quickly as possible, make sure you read all the requirements your chosen provider lists and respond to any requests promptly.

How much does it cost to open an international bank account?

Some providers will charge a fixed fee for managing your account overseas, and many will have a minimum deposit and account value. You may also find you need to have a minimum income being paid into your account, so check the individual terms and conditions of your chosen provider.

Do I pay tax overseas if I have an international bank account?

If you’re a US citizen, income earned overseas is taxable, but opening a bank account overseas does not make you liable to any additional tax. However, the Internal Revenue Service (IRS) and US Treasury have a very rigid declaration process for assets held in foreign accounts.

If the total sum of your finances in international bank accounts is more than $10,000, you’ll need to report this to the US treasury as a Foreign Bank and Financial Accounts Report (FBAR). If the total is more than $50,000, you’ll also need to to file a Foreign Account Tax Compliance Act (FATCA) report with the IRS.

Reporting international bank account balances

US regulations require you and your bank to report details of your account to the US government under certain circumstances. The most common of which are as follows:

If your total account balance across all foreign accounts reaches $10,000 or more, you’ll need to file a Foreign Bank and Financial Accounts Report (FBAR) with the US treasury.

If the total across all your foreign accounts reaches $50,000 or more, you’ll also need to file a Foreign Account Tax Compliance Act (FATCA) report with the IRS.

Banks and transfer providers are required to report any transfers exceeding $10,000 to the IRS to help prevent money laundering.

What if I earn income overseas?

The US is one of only two countries globally that uses citizenship-based taxation, meaning all income earned, whether in the US or another country, is subject to American tax laws. This can mean you end up paying tax twice, known as double taxation.

Double taxation

Double taxation can occur if you’re a US citizen living overseas, as any income you earn is taxable by both your home country and the US government. This can seriously affect your finances if you’re living abroad, since you’re essentially paying twice as much tax as you would be if you earned your salary on US soil, or if you weren’t a US citizen.

Avoiding double taxation

Fortunately, there are ways double taxation can be avoided.

Tax treaties

The US has several tax treaties in place with foreign countries to prevent double taxation. The two main types are:

Income tax treaties

Totalization agreements

These treaties help determine which country will tax which sources of income you receive. When sending your US tax return, you should attach a completed 8833: Treaty-Based Return Position Disclosure so the IRS are aware which treaty article you’re using to modify your tax obligations and avoid double taxation.

Foreign Earned Income Exclusion (FEIE)

If you pass the Bona Fide Residence Test or the Physical Presence Test, you can use the FEIE to exclude approximately $100,000 of foreign earned income from your US tax obligations, regardless of which country you live in.

Foreign Tax Credit

The Foreign Tax Credit was introduced specifically to prevent double taxation for Americans living abroad. If you qualify, the IRS will credit you the entire amount of foreign income tax you paid to your host country.

What’s an offshore bank account?

‘Offshore’ is a common term for bank accounts held in a foreign country. They’re also known as overseas bank accounts and non-resident bank accounts.

Is my money safe in an international bank account?

Like the US, most countries have their own financial protection laws that help protect your money from theft or financial crisis, but each law will be slightly different. There may also be specific financial regulators that ensure your funds are protected.

For example, domestic US banks are protected by the Federal Deposit Insurance Corporation (FDIC), which insures your funds up to a maximum of $250,000 per bank. Some domestic banks covered by the FDIC will offer international bank accounts which have the same level of protection, so it’s a good idea to check this when researching.

Regardless of the country you’re opening an account in, it’s important to check the bank you’re registering with is regulated. Regulated banks are confirmed as being legally permitted to manage finances, whereas unregulated banks have no external bodies verifying that they’re doing what they’re supposed to be.

Which banks allow you to open an international or expat account?

We’ve listed the top banks that offer international banking options to help you make your decision. All these banks come with FDIC protection.

Revolut | Best for international banking overall | Hold and spend money in 30+ currencies; Withdraw up to $400 per month with no fee; Open an account without proof of address or credit check |

Wise | Best multi-currency account | Convert money into 50+ currencies at the mid-market rate; Get your own local bank details in the UK, US, Eurozone, New Zealand, Australia, and more |

Citibank | Best for cash withdrawals | Fee-free cash withdrawals at over 30,000 ATMs globally in 20 countries; Hold money in up to 21 currencies in checking accounts; Earn interest on balances over $200,000 |

Charles Schwab | Best for international spending | No monthly fees or minimum balance for checking account; No foreign transaction fees; Unlimited rebates on ATM fees |

HSBC | Best for widest network | Operates in over 60 countries worldwide; Excellent customer service; No foreign transaction fees |

Is an international bank account always the best option?

You may find an international bank account is not quite suitable for your needs. Alternatively, you can send money to your local bank account, meet regular payments to your home country, or send money abroad to friends and family via a specialist money transfer provider.

Money transfer providers offer several benefits that you may be interested in:

Low transfer fees

More competitive exchange rates than traditional banks

Faster transfer times

More payment/withdrawal methods

Moving overseas: Don't forget about tax and pension contributions

At this stage it is important to contact the tax office and pension provider in your home country, to inform them of your move and new overseas bank account. Expats moving permanently overseas may want to learn more about switching accounts and claiming a pension abroad.

FAQs

Can I open a bank account in another country?

Can I open a US bank account overseas as a US citizen?

How can I open an international bank account online?

Can I withdraw money from my US bank account in a different country?

Are digital payment methods an option?

Related Content

Related Content

Contributors

.jpg)