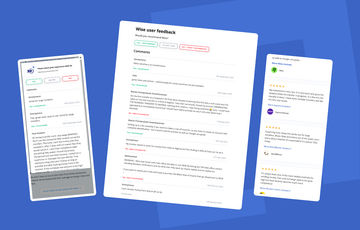

Check the latest reviews & comments to find out what real users think, or add yours.

Setting up is a bit unwieldy if you want to make a one-off transfer, as you have to create an account with complete identification - but it works and the process as well as charges are great.

My experience is very nice. It is very quick and gives the updates while the transfer in progress. In a few min the transfer is done. I have done multiple transfers and did not face any issues.

Surprising how cheap this works out for large transfers. Blows Wise and others out of the water, but I worry about whether it's sustainable? It's almost TOO cheap

It's always been one of the most reliable methods for sending money. Fees and exchange used to be quite high but have recently become much more competitive!

Why Thousands of Users Trust MoneyTransfers.com Comparison Every Week

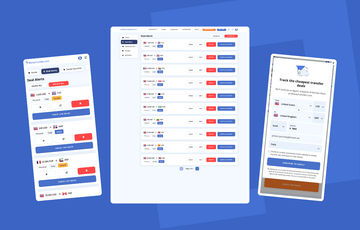

30,000+ live deals scanned daily

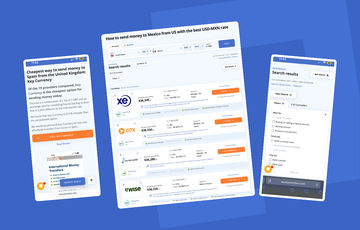

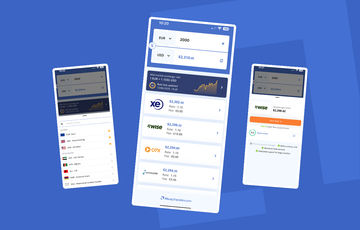

Covering 150+ countries, 80+ currencies and 50,000+ corridors, giving you comprehensive and accurate comparisons. We even have access to exclusive deals from some providers.

Live API connections

Real time deals from money transfer providers like Wise, XE, Global66, WorldRemit, Airwallex and many more

Filter & sort

View your search results by payment method, features & use cases, instantly view fees, rates and transfer speeds, then sort by what matters most to you

Wide banking method support

Support for funding transfers using bank transfer, debit card and credit card, with payout options including send to bank, send to card, mobile money & cash collection

Send from $/£10 to $/£1million+

From remittances to the largest transfers, we have options for all - even offering advanced features like forward contracts, limit orders and hedging for six, seven and eight figure transactions

Comprehensive

We want to give you a full view of the market, including hundreds of money transfer companies. We don't let commercials or partnerships stop us from including companies on our pages. For us, being comprehensive is key.

Focus on financial education

Knowledge is power - MoneyTransfers.com empowers users to understand the world of currency and payments, with tips and guides integrated throughout the experience

Notifications

Create custom notifications for the latest money transfer deals by email, and be alerted when market movements affect the currencies that matter to you

Real insights & reviews

Unbiased review scores plus comments from real users give you a transparent understanding of company strengths and weaknesses

Free membership benefits

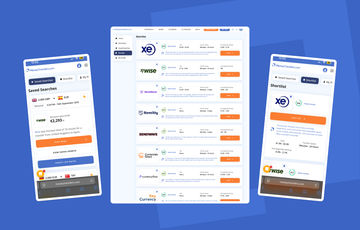

Create a free account to save searches, shortlist companies and manage email alerts

Unique MoneyTransfers.com mobile app

iOS and Android apps for currency conversion & money transfer deals

Business FX solutions

Dedicated search results for business users seeking competitive spot FX transfers or wider currency platform integrations

Get access to today's best exchange rates by filling in the form below.

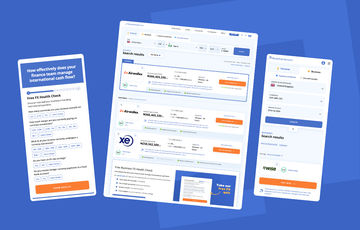

How Effectively Do You Manage International Cash Flow?

In our experience, there are always efficiencies to be made in how businesses manage international payments in and out. Why not take our free FX health check test to see how effective your business is in managing these. It only takes a couple of minutes.

1

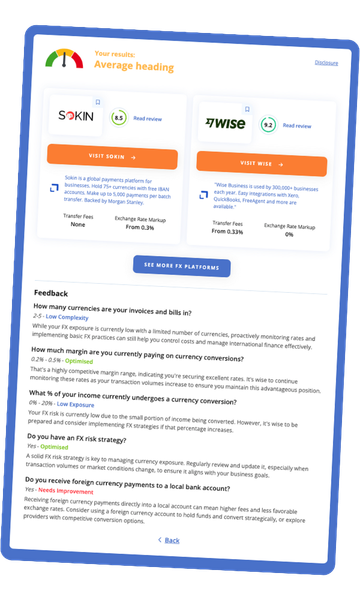

Disclosure

MoneyTransfers aims to help users find the best money transfer provider for their needs. To support our free service, we may earn a commission from some of the providers listed in our search results. The commission may also impact the ordering of the providers shown. Our reviews are independent from this and are based on our editorial policy, research and testing of dozens of remittance providers on the market.

MoneyTransfers aims to help users find the best money transfer provider for their needs. To support our free service, we may earn a commission from some of the providers listed in our search results. The commission may also impact the ordering of the providers shown. Our reviews are independent from this and are based on our editorial policy, research and testing of dozens of remittance providers on the market.

Founded in 2019, MoneyTransfers.com is designed to transform the way you discover the best and cheapest deals when sending money across the world.

We believe transferring money between countries should be a quick and painless experience for everyone involved.

Our mission is to help individuals and businesses navigate the world of international money transfers with confidence, by providing transparent comparisons, real-world testing, and expert insights you can trust.

Read below for answers to the most commonly asked questions.

What is an international money transfer?

An international money transfer involves transferring money from one country to another. The amount of money the receiver receives will depend on the exchange rate at the time of sending the funds.

Why should I use an international money transfer provider to send money abroad?

Money transfer providers are cheaper, faster, and easier to use for international money transfersthan high street banks. They can offer lower fees as they don't rely on the SWIFT network, but use their own network of banks to transfer money.

Transfer providers are also highly regulated, and many offer encryption on your transfers to keep your finances safe.

What problems or issues could arise when sending money abroad?

While most international transfers go smoothly, there are scenarios where things can go wrong. Examples include delays, changes in exchange rate, intermediary bank fees, and transfers being flagged due to size for enhanced KYC.

No. MoneyTransfers.com is a comparison website aiming to match you with the best money transfer providers for your needs when transferring money online.

Can I trust MoneyTransfers.com?

Yes. We compare and review the top money transfer providers on the market to find you the best deal on your transfer. We score providers based on the cost and speed of their transfers, as well as the range of services they offer, and much more.

We pride ourselves on our objective reviews, maintaining complete independence in our analysis and ratings.

Take a look at our comprehensive editorial policy for more information about our dedication to integrity and transparency.

Compare Money Transfer Rates

Get access to the lowest rates by filling in the form below

Search Now & Save On Your Transfer

Instantly view live exchange rates, fees & features.

.svg)

.png)

.png)

Please share your experience with …