SEPA Transfers

SEPA refers to the Single Euro Payments Area, an initiative launched in 2008 to make it easier for people to make international bank transfers in Euros. SEPA is compiled of 36 countries, including all 27 member states of the EU and these countries can transfer money between each other via a dedicated system. This system is designed to be more efficient than the SWIFT network which is generally used for sending money overseas. In this handy guide, we’ll run through the basics of SEPA, outlining everything you need to know and how SEPA can benefit individuals sending money to another country.

Search Now & Save On Your Transfer

What is a SEPA Transfer?

A SEPA transfer is an international transfer made through the Single Euro Payments Area (SEPA), a European Union (EU) initiative for harmonising payments across Europe. The goal is to simplify cross-border money transfers in Euros. In several ways, a SEPA transfer is similar to a domestic transfer (or BACS transfer in the UK), as the banks that support SEPA payments either have direct relationships with other banks or a network of intermediary banks, enabling seamless transfers across international borders.

Within SEPA transfers, the European Payments Council (EPC) has created different SEPA payment schemes to match the various needs of people looking to use the network. These are SEPA Direct Debit (which includes both a ‘core’ and a ‘B2B’ service) and SEPA Credit Transfer.

The countries within SEPA are:

Austria | Latvia |

Belgium | Lichtenstein |

Bulgaria | Lithuania |

Croatia | Luxembourg |

Cyprus | Malta |

Czech Republic | Monaco |

Denmark | Netherlands |

Estonia | Norway |

Finland | Poland |

France | Portugal |

Germany | Romania |

Gibraltar | San Marino |

Greece | Slovakia |

Hungary | Slovenia |

Iceland | Spain |

Ireland | Sweden |

Italy | Switzerland |

SEPA Direct Debit

SEPA Direct Debit is a pull-based payment method that allows a creditor or merchant to debit a debtor/consumer's bank account, provided the debtor has signed a valid mandate to allow the merchant to withdraw the money. SEPA direct debit is exclusively available in Euros, and the payee must have the payer’s International Bank Account Number (IBAN) to collect a SEPA payment. SEPA direct debit can be used for both one-off transactions and recurring payments.

SEPA Direct Debit is a suitable way to pay rent, subscriptions, insurance premiums and other expenses. It is also an effective way for businesses to settle their financial obligations and manage cash flow if moving money abroad.

SEPA Direct Debit Core and SEPA Direct Debit B2B

SEPA direct debit comprises two schemes:

SEPA Direct Debit Core

SEPA Direct Debit B2B

While the Core direct debit scheme is mandatory for all SEPA banks that offer Euro-denominated direct debits, the B2B service is an optional scheme. It is only available to those collecting payments from other businesses.

The main differences between SEPA Direct Debit Core and SEPA Direct Debit B2B schemes is as follows:

SEPA Direct Debit B2B scheme can be used when the debtor is a business or enterprise, while the core scheme is available to both private individuals and enterprises

Some banks do not accept SDD B2B; acceptance is not mandatory

Under the B2C scheme, the payee has to submit the collection request at least 5 banking days before the payment due date and at least 2 days in advance for any subsequent payment collections. On the other hand, under the SEPA B2B scheme, the request has to be submitted only 1 working day before the payment is due. This means that for a cross-border SEPA direct debit payment in the quickest possible way, the B2B direct debit scheme is the right choice.

The B2B scheme mandates debtors to sign an agreement with their bank before any direct debit payments. If the debtor fails to notify the bank, the direct debit will be rejected.

B2B scheme customers are not entitled to refunds while Core scheme customers can seek a refund within 8 weeks for authorised collections and 13 months for unauthorised collections (the debtor needs to provide proof that the creditor was not authorised.)

SEPA Credit Transfer

The SEPA credit transfer service is an interbank payment scheme that defines a common set of standard procedures and rules for credit transfers in Euros.

SEPA credit transfer transactions can be one-off or recurring payments, and can also be made individually or in bulk (payroll, for example, which involves one debit from the payer’s account and multiple credits to different beneficiaries).

Key features of SEPA Credit Transfers include:

The payer, payee and their banks are identified using the International Bank Account Number (IBAN) and Business Identifier Code (BIC)

The beneficiary receives the funds within one business day after the payment is executed

The beneficiary receives the full amount; there are no hidden costs

The cost of a SEPA cross-border payment will be the same as the cost of local transfer

The payer and payee using the SEPA Credit Transfer scheme are only charged by their own service providers for payment

SEPA Instant Credit Transfer

SEPA Instant Credit Transfer, also known as SEPA Instant Payment, enables instant crediting of payees in less than ten seconds. The scheme is available to customers in eight Eurozone countries: Austria, Estonia, Germany, Italy, Latvia, Lithuania, the Netherlands and Spain. SEPA Instant Credit Transfer enables the crediting of payees in less than ten seconds, up to a maximum of €15,000.

Pros and Cons of SEPA Transfers

The core benefits of SEPA payments are simplicity and cost-effectiveness. It lets consumers use one payment account to make euro payments anywhere in the SEPA zone. The only major drawback is its limited access, as payments through the network are only possible in Europe. Here is a closer look at the pros and cons of SEPA payments.

Pros

Cons

How Much do SEPA Transfers Cost?

You pay the same cost for a SEPA transfer as you would pay for a domestic wire transfer, which is zero in most cases. Some banks may charge a nominal fee, so it is important to check with your bank just in case. There cannot be different charges levied based on bank location. This means, if you are making a transfer from your UK bank account, you will pay the same price whether you send funds to a UK account or a Swedish account.

How Do SEPA Transfers Work?

A SEPA bank transfer is similar to a domestic transfer. Here is an example on how SEPA transfers work:

Assume that Sarah is sending Aaron €100, and both sending and receiving banks are part of SEPA. When Sarah initiates the transfer, Sarah’s bank will debit €100 in her account. Sarah’s bank will then credit the recipient’s commercial account held with the sender’s bank by €100. Aaron’s bank will credit his personal account with €100.

In case both the banks do not have an established relationship, as they had in the above example, the transaction will occur through a central bank account/intermediary account in Europe. Therefore, once Sarah’s account has been debited, her bank will credit the amount in the intermediary bank, which will in turn credit Aaron’s bank with €100. Finally, Aaron’s bank will credit his account with €100.

Basically, SEPA transfers work just like a regular bank transfer, only the money is transferred overseas and exclusively in Euros.

How to Make a SEPA Transfer?

SEPA utilises each person’s International Bank Account Number (IBAN) to enable transfers between different bank accounts. To make a SEPA payment, you will need:

The IBAN of the person you are sending money to

To make sure that the bank which you are sending money to is a member of the SEPA

To make a SEPA bank transfer, you need to log in to your bank or payment provider account and set up the transfer as you normally do. Add the recipient by providing the required details, add the IBAN of the recipient’s bank account and pay for your money transfer. The bank or transfer provider will pay the recipient in Euros.

SEPA Transfer Time

SEPA guarantees completed transfers within 48 hours or less during banking days, but it is often quicker compared to bank wire transfer times. The payments made through the SEPA usually take 1 - 24 hours. The domestic SEPA transfers are cleared several times in a day, so the funds are transferred in a matter of hours.Most overseas SEPA bank transfers get credited the following morning, as long as the payment is made before 5 PM and both days fall on business days.

Can I Send Multiple Currencies Using SEPA Transfers?

All SEPA transactions must be in Euros, even if the relevant accounts are not in Euros. If a currency exchange is required, it is up to the banks of the payee and payer and the fees they charge for this service. There may be a cost involved and this may be presented in the form of an exchange rate mark-up or fixed fee.

SEPA vs. SWIFT Transfers

The Society of Worldwide Interbank Financial Telecommunication (SWIFT) is a system of financial messaging which runs on the network of banks and financial institutions from across the globe. It enables institutions to send and receive information on financial transactions in a standardised and secure way using SWIFT code for international money transfers. SWIFT enables money transfers from one bank to another across the globe and in multiple currencies.

While SEPA and SWIFT bank transfers have the same objective, there are some major differences. SWIFT enables money transfers across the globe, but SEPA payments can only be made within the SEPA area, SWIFT transfers can be executed in numerous currencies while the SEPA initiative encompasses Euro transfers alone. Moreover, SEPA transfers involve no or minimal fees, while SWIFT transfers may cost anywhere between $15 and $45.

Generally speaking, SEPA bank transfers are more hassle-free as you only need the IBAN to make the transfer. To make a SWIFT transfer, you need the name of the recipient, IBAN, BIC, SWIFT code, the beneficiary address, and bank details, account number/branch code and specific currency.

More SWIFT Guides

Summary

SEPA enables anyone who holds an account with a bank, or other payment service provider located in the countries covered by the SEPA, to send and receive Euro-denominated payments to and from accounts anywhere else in the SEPA.

SEPA has two schemes available to residents of participating countries: SEPA Credit Transfer and SEPA Direct Debit. SCT enables credit transfer service within the participating countries and very fast transaction speeds, while SDD allows consumers and businesses to make cross-border direct debit payments in Euros, with transfers usually taking in the region of 2 days to be completed.

The SEPA Direct Debit service is further divided into SEPA Core Direct Debit and SEPA B2B Direct Debit. The main target market for Core Direct Debit scheme is private and retail customers, whereas the B2B service enables direct debits between enterprises. Every bank within the SEPA area accepts transactions using the Core Direct Debit network, whereas the B2B service is optional and not offered everywhere.

Essentially, SEPA was designed to make international transactions within Europe as seamless as domestic bank transfers. The network allows fast, low cost transfers across the continent, and the only fees you’ll have to worry about are exchange rate margins for those trying to send money in a currency other than Euros (e.g. GBP).

Cheaper Alternatives for International Transfers

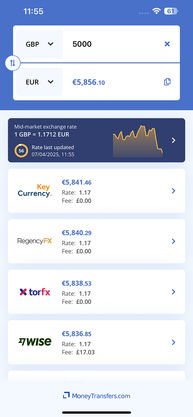

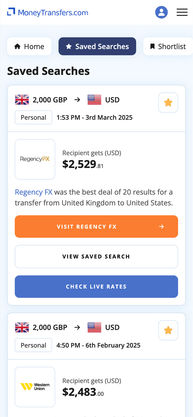

SEPA transfers are a decent way of sending money, but not the best. To save money on transfer fees, you need to go with specialist transfer providers. They charge the lowest fees in the industry and offer FX rates that match the mid-market rate. You can see the rates for yourself by checking out the comparison engine.

To save time on research, you can start sending money with Wise. Their variable rate fee structure is ideal for sending small amounts of money. Also, they consistently offer the best FX rates in the industry. Therefore, you will save money on transfers compared to banks. Wise is a transparent service, so you can see the fees ahead of time and there are no hidden charges.

Related Content

Related Content

Contributors