.svg)

What is mobile money?

Mobile money is a digital or electronic service you have on your smartphone or tablet, often linked to your mobile number or email address. Mobile money services can function a little like bank accounts, letting you manage your finances through your mobile device rather than having to go to a physical bank.

What can you do with mobile money?

Most mobile money services allow receiving and sending money to peers, as well storing it in a virtual wallet on your device or withdrawing and depositing at authorised agents. Your wallet can be used to purchase goods and services online or in-store, pay bills, and most other things you can use a debitor credit card for.

A mobile money transfer is a way to send money via mobile money app or service, either to their mobile phone or another receiving method like a bank deposit or cash pickup.

How long do mobile money transfers take?

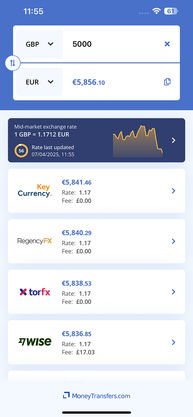

One of the biggest benefits of mobile money transfers is that they are often instant - but this often comes at a steep cost. Here’s how long it takes with some of the biggest mobile money providers:

Provider | Transfer speed |

|---|---|

PayPal | Instantly available in balance |

Cash App | Instantly available in balance |

WorldRemit | Within minutes |

Remitly | Minutes with Express transfers, 3-5 days for Economy transfer |

How much do mobile money transfers cost?

The downside with many mobile money networks is that they can charge higher fees than alternatives like money transfer providers. Here are the fees for some of the biggest mobile money companies:

Provider | Transfer fees |

|---|---|

PayPal | 5% of transfer fee (Min $0.99 max $4.99) |

Cash App | No fees but only transfers between US and UK |

WorldRemit | Between $1.99 and $3.99 |

Remitly | Depends on country and currency |

Is mobile money safe?

Mobile money providers are subject to the same local financial regulations as banks and other financial institutions. Users are required to undergo identity checks, like with money transfer providers, and all transactions are recorded and stored safely.

Providers employ strict data protection measures to keep your money and data secure. You may have to go through extra security steps on your first money transfer as part of extra security protocols before you can start sending money.

How do mobile payments work?

Mobile payments are simple and straightforward, often taking minutes to complete:

How to send money abroad with my mobile

To transfer money abroad via your mobile, you’ll just need to do the following:

Sign up

Link bank account

Send money

Add recipient details

Confirm details

How to receive a mobile money payment

To receive money to your mobile wallet, you’ll need to do the following:

Sign up

Register with your chosen provider with your name, address, phone number and email, and verify your identity

Link bank account

To withdraw money from your mobile wallet you’ll need to link an account with your bank

Give sender your details

Ensure the sender has your username, email or phone number correct so they can send you money

Withdraw money

Once you receive the money into your mobile wallet, withdraw it either into your bank account or as a cash pickup

What countries accept mobile money payments?

Many countries in Africa and Asia have mobile network providers that have partnerships with money transfer services, as well as some places in the Americas and Oceania. In these places many people have mobile money accounts that allow them to send money directly to their mobile phone. As such it’s common to find mobile money transfers from the USA to Nigeria or from the USA to Ghana.

Mobile wallets that partner with money transfer providers aren’t especially common in Europe or the Middle East. However in these locations you can get money to a mobile phone via money transfer providers like Wise.

Who are the most common mobile money providers

Some of the most common mobile money providers include:

Vodafone

Orange Money

Google Wallet

Samsung Pay

Apple Pay

Walmart Pay

There are also many region-specific mobile providers that operate in either one or a few select countries, such as:

Name | Country | Name | Country |

|---|---|---|---|

Airtel | India | helloCash | Ethiopia |

bKash | Bangladesh | JazzCash | Pakistan |

Coins.ph | Philippines | Link Aja | Indonesia |

Dana | Indonesia | M-Pesa | Kenya, expanded to Tanzania, Mozambique, DRC, Lesotho, Ghana, Egypt, Afghanistan and South Africa |

DaviPlata | Colombia | Movii | Colombia |

EasyPaisa | Pakistan | MTN Mobile Money | Ghana and much of Africa |

Equitel Money | Kenya | Paga | Nigeria |

eSewa | Nepal | PayMaya | Philippines |

EZ Cash | Sri Lanka | ShopeePay | Thailand |

GCash | Philippines | Tigo | Colombia and much of South America |

Gopay | Indonesia | UPaisa | Pakistan |

GrabPay | Singapore | UPay | Bangladesh |

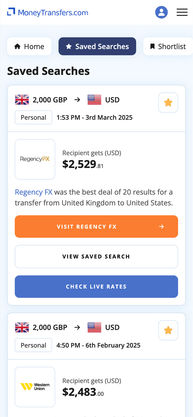

What money transfer providers let you send money to mobile wallets?

Provider | Countries |

|---|---|

Asia: Bangladesh, Indonesia, Nepal, Pakistan, Philippines, Sri Lanka Europe: Armenia Américas: Ecuador, El Salvador, Guatemala Africa: Burundi, Cameroon, Congo DRC, Ghana, Kenya, Lesotho, Malawi, Rwanda, Somalia, Somaliland, Tanzania, Uganda, Zambia, Zimbabwe Australia and Oceania: Fiji, Samoa, Tonga | |

Ghana, Kenya, Senegal, Bangladesh, India, Philippines and Colombia | |

Supports sending money to mobile providers in over forty countries but weren’t able to provide a complete list | |

Allows transfer to digital wallets in over thirty countries around the world, from over forty countries | |

From the US to digital wallets in Bangladesh, Cambodia, El Salvador, Gabon, Guinea, Ivory Coast, Malawi, Mozambique, Senegal, Tonga, Zambia, Botswana, Cameroon, Ethiopia, Ghana, Guinea-Bissau, Kenya, Mali, Philippines, Sierra Leone, Uganda, Zimbabwe, Burundi, China, Fiji, Guatemala, Indonesia, Madagascar, Mongolia, Samoa, Tanzania and Vietnam |

Benefits and drawbacks of mobile money

It’s important to consider the pros and cons of using a mobile money app or service before deciding which, if any, is right for you:

The benefits include:

Convenience: Having money available 24/7 on a device without having to carry around cash or visit a physical branch is useful, especially in rural communities or areas without a developed banking infrastructure

Speed: Mobile money payments are often instant and take a few minutes at the most to clear, much quicker than bank transfers

Security: Mobile providers use advanced security protocols to ensure your personal data and information is all kept safe and protected

No bank details: To send and receive money you’ll often only need to give an email address or phone number, rather than bank account details

The drawbacks include:

Transfer fees: Mobile money apps like PayPal have high fees for international money transfers, compared to providers like XE and WorldRemit

Withdrawal fees: You often have to pay an extra fee to withdraw money from your mobile wallet to your actual bank account or as cash

Limited range: Not all places or countries accept mobile wallets, so they’re more often than not only useful locally

Vulnerable to tech issues: Like with any mobile or electronic service these apps can be vulnerable to tech issues and bugs that can leave you without access to money

Types of mobile money

Mobile money is a term that can be used to describe a range of services, such as:

Digital wallets (Apple Pay, Amazon Pay, Samsung Pay, Google Pay)

Digital wallets are apps that store your debit and credit card information virtually, and you can use them in the same way - to make payments and purchase goods and services. Some even let you send money to other users - but these services aren’t available in all locations.

For example, you can only use Google Pay in the US to send money to India and Singapore.

Mobile money apps (Cash App, PayPal, Venmo, Zelle)

Mobile money apps are more of a universal application, that allow you to send money to peers, and have a built-in digital wallet as part of the service. PayPal even lets you send money across international borders to other PayPal users, though it comes with a steep transaction fee. Cash App only operates between the US and the UK, allowing domestic and international payments between the two.

Keep in mind that when using one of these providers, you will likely have to pay an extra fee to withdraw the money back into your actual bank account.

Money transfer providers (WorldRemit, Wise)

Money transfer providers are a modern solution to international money transfers, and many of them are available on convenient and easy-to-use apps. For example, Wise lets you send money at low rates and fast speeds, while also offering a multi-currency wallet in which you can keep money.

Many providers also allow sending money via digital wallet to recipients all over the world. They can then receive the money in a bank account, for a cash pickup, or if available a deposit to their own mobile wallet.

Airtime top up

Mobile money can also refer to airtime transfers, where you send money to the recipient in the form of airtime. This is usually either talk time i.e. minutes for phone calls, or mobile data for internet browsing.

SMS mobile pay

While not prevalent in the US, many parts of the world have the ability to pay for goods and services by SMS or text message from their mobile phone. Examples of providers who offer this are M-Pesa and Orange Money.

Mobile banking

Many traditional banks have developed mobile banking services that let you access your account and most products via your mobile phone. However domestic wire transfers can cost around $25 and international around $30-50 for sending money, and $15 for any kind of incoming transfer.

These high charges are still present in mobile banking, which is why many in the US still prefer to use apps like Zelle and Venmo.

Bank | Mobile international transfers | International transfer fee | Transfer time |

|---|---|---|---|

Bank of America | Yes | $45 for outgoing US dollar transfers | 3-5 days |

Wells Fargo | No | Undisclosed | 1-3 days |

Chase | Yes | $40 | 3-5 days |

PNC | Yes | $40 | 2-3 days |