International Bank Transfer Fees

A bank transfer, also known as a wire transfer, used to be the default way to send money abroad, but their high fees and long transfer times are falling behind competitors like money transfer providers. Here are the fees for international wire transfers for some of the biggest banks and financial institutions in the world - see how they compare.

Search Now & Save On Your Transfer

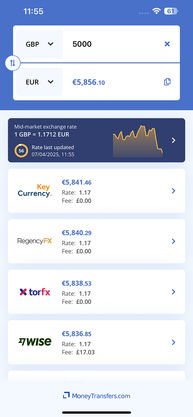

International bank transfer fees vary by bank and location, often ranging from $15 to $50 for outgoing transfers, plus potential intermediary fees and exchange rate markups. Banks tend to be more expensive and slower than money transfer providers, which offer competitive rates and faster transfers.

"Over 15 million customers use Wise, mostly for their excellent mobile app, transparent fee structure & use of mid-market rates. Now increasingly used for larger transfers."

"Over 15 million customers use Wise, mostly for their excellent mobile app, transparent fee structure & use of mid-market rates. Now increasingly used for larger transfers."

"Over 15 million customers use Wise, mostly for their excellent mobile app, transparent fee structure & use of mid-market rates. Now increasingly used for larger transfers."

How much do international bank transfers cost?

International wire transfer fees in the US can range between $25 and $45, depending on the bank, while some banks also charge different fees for outgoing and incoming wire transfers. MoneyTransfers.com has looked at the biggest banks in the US, the UK and around the world to see how much they charge for international wire transfers:

PNC wire transfers

Bank of America wire transfers

Chase wire transfers

Citibank wire transfers

Capital One wire transfers

Wells Fargo wire transfers

USAA wire transfers

Schwab wire transfers

Truist Bank wire transfers

HSBC wire transfers

Barclays wire transfers

Lloyds wire transfers

Natwest wire transfers

Santander wire transfers

If you’re making an international wire transfer within certain countries in Europe, law dictates that your bank must charge the same rate as they would for a domestic transfer. This applies to all countries in the SEPA (Single Euro Payments Area), a network in Europe that allows sending euros within this zone.

There are 36 member states in SEPA, including 27 from the EU, plus a handful of others. The UK is still a SEPA member despite leaving the EU.

Here are the bank transfer fees for some of the biggest banks in Europe:

Deutsche Bank AG wire transfers - Germany

BNP Paribas wire transfers - France

UBS Group AG wire transfers - Switzerland

Canada

Australia

What are international wire transfer fees

There are a few different types of fees for international wire transfers to be aware of, and we’ve listed them below:

Fee | Definition | Example price | Charged by money transfer providers? |

|---|---|---|---|

Outgoing wire transfers | This translates to the basic transfer fee for sending money abroad from your bank account | $15-40 | Sometimes - usually much lower |

Incoming wire transfers | This is the fee the recipient will have to pay to receive money sent from abroad into their bank account | $10-20 | No |

Corresponding or intermediary bank fees | This is what intermediary banks charge during the transfer when money is sent through these banks as part of the SWIFT network | $5-15 per bank | No |

Initiation or setup fee | This is what you’ll pay for essentially setting up the transfer, and it often applies if you set the transfer up by phone, while it’s often waived if you set the transfer up online | $5-10 | No |

Tracer fee | The tracer fee is the cost of tracking the status or progress of your international money transfer | Up to $50 | No |

Exchange rate markups | While the mid-market exchange rate determines the overall worth of your currencies, banks will add their own markup as another way of making money out of the transaction. They often add higher markups than money transfer providers, too | 4-8% of total transfer amount | Sometimes - usually much lower |

What affects the cost of international bank transfers

The cost of your international wire transfer can be affected by factors like:

The type of transfer you’re making: Some banks offer premium transfers that occur much faster, but often come at a higher cost

The currencies involved: Different banks may offer different charges based on the currencies involved in the transfer

Banks vs money transfer providers

If you want to avoid wire transfer fees, your best alternative is to use a money transfer provider. These companies specialise in sending money abroad at low rates, using a network of bank accounts around the world to move money while avoiding the SWIFT network.

Money transfer providers | Banks | |

|---|---|---|

Fees | Transfer fee and/or exchange rate markup | Sending fees, receiving fees, intermediary fees, setup fees, tracer fees, exchange rate markup |

Speeds | Varies, but can be as quick as minutes | Often more than a day or two |

Transparency | When you compare with MoneyTransfers.com you’ll be able to see all transfer fees, as well as the rate you’ll get from the provider, and the exact amount the receiver will get | Banks are not always transparent with their wire transfer fees, and this can be particularly true with exchange rate markups |

Security | Money transfer providers on MoneyTransfers.com are authorised and regulated by the appropriate authorities to provide money transfer services | Banks are also regulated and authorised by the same organisations, and people have been using banks for centuries to manage their money |

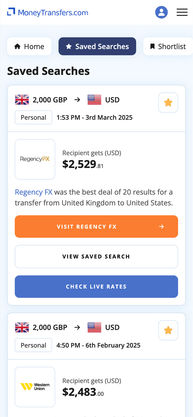

Here’s how money transfer providers compare to the banks when sending money abroad:

Sending $2,000 from the USA to Mexico

Exchange rate on 15/05 - 17.56

Provider | Fees | Exchange rate | Transfer time |

|---|---|---|---|

Chase | $5 & 7.6% above MMR | 16.23 | 2-3 days |

Wells Fargo | $30 & 7.89% above MMR | 16.18 | 3 days |

WorldRemit | $1.99 | 17.31547 | Minutes |

Instarem | $1 | 17.4016 | 1-2 hours |

Sending $10,000 from the USA to Canada

Exchange rate on 15/05 - 1.35

Provider | Fees | Exchange rate | Transfer time |

|---|---|---|---|

Bank of America | $50 & 6.56% above MMR | 1.2604 | 2-3 days |

Capital One | $30 & 7.35% above MMR | 1.2498 | 2-3 days |

Currencies Direct | $0 | 1.3428 | 1-2 days |

TorFX | $0 | 1.3312 | Within 24 hours |

Sending $100,000 from the USA to India

Exchange rate on 15/05 - 82.24

Provider | Fees | Exchange rate | Transfer time |

|---|---|---|---|

Chase | $0 & 8.3% above MMR | 75.37 | 2-3 days |

Citibank | $12 & 4.3% above MMR | 78.74 | 2-3 days |

Wise | $689.49 | 82.2515 | In seconds |

XE | $0 | 81.8288 | Within minutes |

Why are banks so expensive?

International wire transfers with banks are one of the most expensive ways to send money abroad due to their reliance on the SWIFT banking system. When you send money via an international bank transfer, your bank uses the SWIFT network to communicate with the recipient bank, confirming details about the transfer.

Once this step takes place, your bank sends the money through a series of intermediary banks before it ends up at the receiving bank. Each of these banks takes a fee, on top of all the other fees you have to pay to your bank - and they all add up.

Because most banks have a range of other products and services on offer, they don’t generally dedicate many resources to international transfers. As a result it remains an expensive way to send money abroad, often including high wire transfer fees.

This is where money transfer providers changed the game. These online-first companies that focus almost exclusively on remittance are able to offer cheaper transfers using their significantly more streamlined infrastructure.

How do money transfer providers work?

Money transfer providers use their own network of bank accounts across all the countries in which they operate. When you make a domestic bank transfer to your chosen provider, they simply credit the same amount - minus fees and exchange rate markups - from a bank account in the receiving country to the recipient’s account. No money ever crosses an international border, so the only fees to pay are to the provider.

What is the cheapest way to send money internationally?

Money transfer providers routinely offer the cheapest way to send money abroad - it’s just a case of finding the right provider for the transfer that you want to make. Comparing your options with MoneyTransfers.com is a quick and easy way to find the best deals available for your transfer.

Cheapest for | Provider | Average Fee | Send Money |

|---|---|---|---|

👪 Regular payments home | Wise | 0.40% | |

🏡 Property purchases | Key Currency | 0.2 - 0.7% | |

🏦 Bank transfers | XE | £0 | |

💵 Cash pickups | World Remit | $1.99 | |

🚀 Instant money transfers | World Remit | $1.99 | |

📱 Mobile payments | Atlantic Money | $3 | |

👔 Business Payments | TorFX | 1 - 2% |

In most cases, the cheapest way to send money abroad will be by using a money transfer provider and paying by bank transfer. As explained above, this often results in the lowest fees and the best exchange rates - however, just be aware that bank transfers can sometimes take a little longer to process than other methods.

How to save money on your international bank transfer

If you want to make an international money transfer from your bank to another bank account overseas, here are MoneyTransfers.com’s recommendations for getting the cheapest deal possible:

Online not phone/branch: Many banks will charge a smaller wire transfer fee if you transfer money online or via an app, compared to over the phone or in-branch

Avoid using credit or debit card: Using your credit card to fund an international transfer will incur a range of fees, including a cash advance fee, a currency conversion fee and possibly even interest payments. Debit cards aren’t as expensive but their currency conversion fees are still often higher than you’d get with a money transfer provider

Sacrifice speed: As is the case with so many things, you’ll find that the faster you want your transfer to happen the more you’ll need to pay. If you can afford to wait a while, it’s likely there will be a cheaper option available that will take possibly two or more days to complete

Use a money transfer provider: The easiest and most reliable way to make an international bank transfer is to use a money transfer provider. With MoneyTransfers.com you can compare rates from the biggest providers in the industry, like WorldRemit, Wise and XE - so you can see who offers the fastest and cheapest bank transfers to your chosen destination

Is it possible to make a free international bank transfer?

It’s unlikely that you’ll be able to make a free international bank transfer as there will always be some kind of charge involved. A notable exception is if you live in the SEPA zone.

FAQs

How long does a bank transfer take?

When are international bank transfers useful?

What is the difference between a wire and bank transfer?

Are bank transfer fees tax deductible?

Do all banks charge transfer fees?

Can bank transfer fees be waived?

Are domestic wire transfers cheaper with banks?

Related Content

Contributors