.svg)

.jpg)

Convert on the go with our currency app

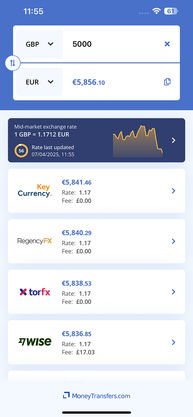

Convert 25,000+ currencies

Get reviews & insights

No ads or subscriptions

Compare live transfer deals

Convert 25,000+ currencies

Get reviews & insights

No ads or subscriptions

Compare live transfer deals

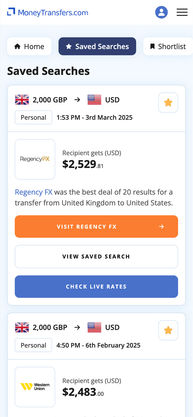

Save your favourite searches

Shortlist providers

Sync between all your devices

Absolutely free