N26 vs Monzo

Comparisons are often drawn between London-based challenger bank Monzo and the Berlin-based equivalent, N26. Both brands are breaking boundaries as digital alternatives to traditional banking services, but we want to know which company is the better option for customers who need to make money transfers?

N26

N26, Europe's first digital bank, is a Berlin-based fintech business founded in 2013 by Valentin Stalf and Maximilian Tayenthal. N26 accounts can be accessed via smartphone app or web browser. The bank has established a presence in over 20 European nations, and has recently moved into the US market, resulting in the N26 customer base amounting to over 6 million people.

The company was granted a banking license by The German Central Bank in 2016 and funds up to €100,000 that are deposited in N26 accounts are covered by the German Deposit Guarantee Scheme. Following its series D round of funding in May 2020, the company was valued at $3.5 billion.

Monzo

Monzo was founded in 2015, set up by five former colleagues who met while working at competitor challenger bank, Starling. Together, Tom Blomfield, Jonas Huckestein, Jason Bates, Paul Rippon and Gary Dolman started an app-based neobank aimed at customers looking to make the switch from traditional to digital banking. Starting out life as a prepaid Mastercard and accompanying mobile app, Monzo was originally designed as a type of pay-as-you-go travel card. In response to the notable shift in consumer banking, Monzo began to develop its offerings, evolving into an intuitive alternative banking service. As a result, Monzo has expanded into an FCA approved bank offering a wide range of UK accounts as well as loans and overdrafts.The bank partnered up with Wise, one of the biggest and most reputable money transfer companies on the market, in 2018. Since then, Monzo has continued to concentrate their efforts on improving their global payment services.

About N26 and Monzo

Challenger banks, also known as neobanks, are a type of banks that are shaking up the status quo by operating exclusively online or without the traditional expectations of long-established large national banks. They are set up to compete with the bigger banks, by providing more accessible and convenient online alternatives to traditional banking services. Both banks cut overhead costs by operating purely online, removing the need for physical bank branches and saving money in the process.

N26 is located in Germany and was designed to be a mobile bank that is transparent, flexible and customer-focused. The company’s commitment to these three pillars of business is evident in the user-friendly design of the N26 app, the cutting-edge technology used to streamline financial services and the clear and concise approach to fees and terms of use.

Monzo serves the same market and purpose as N26, albeit a British-based version. Committed to providing clear and convenient digital alternatives to everyday banking, Monzo has become a staple peer-to-peer payment platform for UK customers, with its trademark neon pink debit card widely used as a fully licensed UK bank account.

N26 and Monzo have many great qualities and there are numerous reasons to bank with both companies. For this comparison, however, we will be evaluating how easy it is to send and receive international money transfers with both brands, reviewing the total cost, speed and exchange rates offered by each.

Which brand has lower fees?

A great deal of banks and money transfer companies claim to provide a low-cost or fee-free service, but sadly this is not always 100% accurate. Here we will take a closer look at N26 and Monzo fees for international money transfers.

N26 customers can make unlimited overseas card payments and ATM withdrawals fee-free.

It is also free to receive euro transfers from EEA states and Switzerland.

When it comes to sending money overseas, N26 customers can take advantage of the bank’s partnership with money transfer giant, Wise. Global remittances can be set up easily by tapping on the Wise feature which is directly integrated into the N26 app. Wise shares N26 transparent approach to transfer fees, and the overall cost should not amount to more than 0.35 - 0.65% of the total transfer amount.

However, N26 warns customers of transaction processing fees, typically around 2%, which will be charged by the bank or card company that is providing the international service.

In addition to this, any refusal of a direct debit due to insufficient funds will result in a fee of €3.00 per refusal.

Customers can find out more about transfer fees under Foreign Transaction Fees on the N26 website.

Like N26, Monzo has teamed up with Wise to provide low-cost international money transfers powered by experts in foreign exchange. Wise transfer fees are based on the type of remittance service the customer chooses. These options include Low Cost, Advanced or Fast transfer services.

As previously mentioned, Wise fees typically do not amount to more than 0.35 – 0.65% of the transfer amount.

Due to the fact Wise fees are figured out as a percentage of the overall amount, the larger the transfer, the higher the fees.

Monzo makes it easy to review all transfer fees in full, using the app, before making a payment: follow this link to find out more.

✅ Verdict: It’s a tie

N26 and Monzo approach fees in a near-identical way, and given the fact both companies have partnered up with Wise to provide convenient and quick global remittances, it appears similar transfer fees are applied across the board.

Which brand offers better exchange rates?

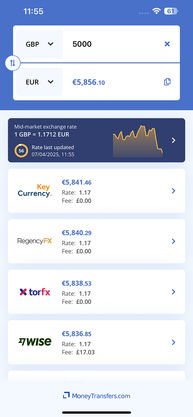

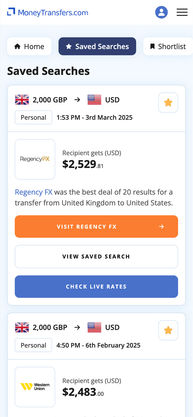

Locking in the most favourable exchange rate will make a huge difference to the value of any cross-border payment.

According to the Foreign Currency Exchange page on the N26 website, the company works together with Wise to provide “the best exchange rates available” for international money transfers.

When it comes to spending overseas, N26 states that the currency conversion fee of around 1% is applied to payments that require conversion from one currency to another.

When arranging international money transfers, Monzo customers will have full access to the transparent exchange rates offered by Wise. This means, in most cases, customers will be offered an exchange rate that closely matches the mid-market rate.

Our research indicates an average exchange rate spread of 0.05 – 0.5% is added to most foreign currency transfers.

✅ Verdict: It is another tie

Considering Wise powers both N26 and Monzo international money transfers, customers of both brands have access to the real mid-market rates, provided by one of the leading authorities in foreign currency exchange.

Which brand covers more locations?

Many money transfer providers claim to cater to a global market but we want to identify how many countries N26 and Monzo services cover.

N26 is available to customers in the following 23 countries; Austria, Belgium, Denmark, Estonia, Finland, France, Germany, Greece, Iceland, Ireland, Italy, Liechtenstein, Luxembourg, The Netherlands, Norway, Poland, Portugal, Slovakia, Slovenia, Spain, Sweden, Switzerland and the US. Controversially, in 2020 N26 announced they would be closing all British customers’ bank accounts and cease to operate in the UK.

As N26 international money transfers are powered by Wise and seamlessly integrated into the N26 mobile app, it is easy for customers to transfer funds to over 38 countries.

Unlike N26, Monzo is exclusively available to customers in the UK. However, thanks to their partnership with Wise, it is possible for users to send money overseas to 34 countries. As a UK based entity, Monzo is included in the SEPA zone, making Euro transfers the easiest and most popular type of international transfer set up by customers.

✅ Verdict: N26 covers more locations

Customers around Europe can register with N26, whereas Monzo is only available to UK-based users. This means N26 is in a better position to accommodate international customers and their global money transfers.

Which is faster?

Transfer speed can be the primary concern for many customers who are sending money online and it is an important factor to consider for any time sensitive transactions.

Transfer speed will depend on the type of international money transfer that is chosen by the customer but, on average, N26 customers report most cross-border payments taking 2 – 3 business days.

Standard SEPA transfers should arrive within a maximum of 2 working days. If the recipient’s bank supports instant credit transfers, they will receive SEPA credit transfers within minutes.

International transfers can take 2 - 3 working days to arrive with the recipient. However, funds sent in standard currencies to popular destinations are typically transferred within 1 working day.

✅ Verdict: Monzo wins here

According to advice on their website and feedback from customers, it seems Monzo offers a slightly faster transfer rate out of the two brands.

Which brand offers more transfer & payment options?

Not all companies can accommodate every kind of transfer or payment and it is crucial to assess the range of options on offer, before choosing a brand to trust with your hard-earned money.

Wise handles international money transfers on behalf of N26 and the transfer options available are as follows:

Fast and easy transfer: the quickest way to send money overseas, paid for using debit or credit card, or a digital wallet like Google Pay. Albeit fast, this option is the most expensive.

Low-cost transfer: this cost-effective option and is ideal for customers prioritising price over speed. This type takes the longest, due to payment via bank transfer.

Advanced transfer: this type of international money transfer utilises the SWIFT network, which typically incurs a fee.

The payment options available with Wise through N26 are:

Credit card

Debit card

ACH direct debit

Bank transfer

Wise handles international money transfers on behalf of Monzo and the transfer options available are as follows:

Fast and easy transfer: the quickest way to send money overseas, paid for using debit or credit card, or a digital wallet like Google Pay. Albeit fast, this option is the most expensive.

Low-cost transfer: this cost-effective option and is ideal for customers prioritising price over speed. This type takes the longest, due to payment via bank transfer.

Advanced transfer: this type of international money transfer utilises the SWIFT network, which typically incurs a fee.

The payment options available with Wise through Monzo are:

Credit card

Debit card

ACH direct debit

Bank transfer

✅ Verdict: Monzo and N26 come joint 1st

The transfer and payment options offered to N26 and Monzo customers are provided by Wise, meaning the options are identical and both brands win this one.

What do users have to say about each brand?

N26 is a German brand, while Monzo is UK-based, but what do their international customers think of their financial services?

This challenger bank’s mobile services are primarily accessible via the N26 application. On the App Store, N26 has been given 4.7 out of 5 stars, and 4.4 out of 5 on the Google Play Store: this suggests Android users may experience more issues with the app, than those who use an iPhone.

Trustpilot provides insight into customer experiences and N26 has been rated as a “Great” company, with 3.9 out of 5 stars. Although this is a respectful rating, 20% of the online reviews are categorised as “Bad” with customer complaints citing issues with standard SEPA transfers, unsatisfactory customer service and long wait times.

Positive comments make up 78% of the Trustpilot reviews for N26, with many customers praising the straightforward, easy to use mobile app and low cost foreign payment services.

As a challenger bank that is exclusively accessible via mobile or smart device, a great way to gauge customer satisfaction is by evaluating reviews of the Monzo app.

Over 60,000 Android users have rated the app 4.7 out of 5 stars, while iOS users have given the app 4.9 out of 5. This suggests the app is well designed and considered reliable by all who use it.

Over on Trustpilot Monzo has been awarded 4.5 out of 5 stars by more than 17,000 users.

Positive feedback accounts for 86% of the reviews, many of which reference the easy to use mobile interface, quick cross-border payments, helpful real-time notifications and spending insights.

Around 12% of the reviews are categorised as Bad or Poor and they include comments about account freezes and closures, blocked funds and unsatisfactory customer service.

✅ Verdict: Monzo wins based on reputation

Judging by reviews posted online, Monzo is more popular with users and the mobile app is more reliable and intuitive. Therefore, at the time of writing it seems Monzo is more likely to attract long-term, repeat customers than N26.

What brand offers better ease of use, accessibility, transparency & security?

We will run through each factor as we evaluate which is the more successful brand when it comes to overall user experience.

Accessibility: N26 caters to multiple international markets and can be accessed in over 20 countries. Despite succesfully registering with N26, Some users have reported issues accessing certain functions when using the app. Also, British account holders were very disappointed when the company abruptly announced it would no longer support UK customers.

Transparency: In terms of the international money transfer services, N26 works alongside Wise, who offer total transparency throughout the entire process of moving money overseas.

Security: In addition to possessing a full European bank license since 2016, customer funds are protected up to €100,000 by the German Deposit Protection Scheme. Additional security settings such as biometric authentication and 3D secure technology are also used to ensure customer data is protected. Customers can review N26 full security terms and conditions here.

Ease of use: Online reviews primarily consist of positive online banking experiences, with many customers dubbing the mobile app intuitive, comfortable and simple to use.

Accessibility: Only customers with a residential address in the UK can access Monzo services, and it is also only accessible in the English language.

Transparency: Monzo customers can benefit from the guaranteed transparency of Wise terms of service, with support accessible via in-app messaging, email or phone

Security: Monzo is covered by the Financial Services Compensation Scheme (FSCS) which means customers’ funds are protected (up to £85,000). In addition to this bank-level insurance, sophisticated data encryption and two-factor authentication is used to further protect customer details.

Ease of use: User consensus is that Monzo is quick and easy to sign up for, learn how to use and manage finances with. The clearly displayed categories make it easy to create tailor made budgets and savings pots, review spending habits and set up domestic or international money transfers.

✅ Verdict: It is another tie

Both Monzo and N26 perform exceedingly well in each category, with both brands covering all bases when it comes to user experience, accessibility, transparency, and safety and security, which means yet another tie.

Additional features

In this section we will be reviewing any perks or bonus features that are offered to N26 or Monzo account holders.

Customers have access to overdraft and loan services

Customers can choose from a range of fun contactless debit cards, available in 5 colors—Ocean, Sand, Rhubarb, Aqua or Slate

Premium membership provides access to Sub-accounts; customers can create 10 Spaces sub-accounts within their main account, as a way to help organise finances and reach savings goals

Exclusive benefits and offers: N26 customers receive exclusive perks with big brand names

Customers have access to overdraft and loan services

Customers can set budgets to monitor their daily, weekly or monthly spending

Saving is easy with Monzo Saving Pots; plus zero interest rates on free savings accounts (up to 1.5% AER on paid accounts)

Low-interest joint accounts are available for couples and junior accounts for 16 – 17 year olds

Customers can switch energy suppliers through Monzo and will be rewarded £50 credit

✅ Verdict: Once again, it is a tie

As innovative challenger banks, both N26 and Monzo work tirelessly to provide useful and enticing exclusive perks and features to their customers. We cannot decide who offers the best additional features so it is once again a tie.

Final verdict: who is better?

After conducting a comparative analysis of these two challenger bank brands, we have come to the conclusion that there is no clear winner. Instead, it appears N26 and Monzo are equally reliable, low-cost and transparent money transfer providers. However, we would recommend different banks to different customers. N26 is the best option for European customers, whereas Monzo is designed for the UK market. This being said, both support fast and secure SEPA transfers.

Both companies have teamed up with Wise to facilitate the fastest, most favourable global money transfers deals on the market. Further to their partnerships with Wise, both challenger banks adhere to financial regulations, implement high-level security protocols and are insured by the relevant governing bodies. If you are still unsure which company to use to send or receive money, we recommend our comparison engine. This invaluable online tool is a great way to compare all the available global remittance options.

Related Content

Related Content

Contributors