Electronic vs Wire Transfers: Compared for Speed, Cost and Safety

Wire transfers and EFTs are often confused, but there are differences between them. EFT is an umbrella term encompassing all automatic electronic transfers, while wire transfers are a specific type of EFT.

In this article, we cover the difference between wire transfers and EFTs, the benefits of each, and how you can choose which is best for you.

How to choose between an EFT and a wire transfer

Both wire transfers and other types of EFTs have their uses, but it will depend on the type of transaction you’re trying to make. Wire transfers hold some advantages over other EFTs, such as the speed of transfer and higher sending limit, but lower costs and extra legal protections are available with other EFTs.

EFTs vs wire transfers - Speed

Domestic wire transfers can be processed instantly, while other kinds of EFT can take longer, making wire transfers a better choice for time-sensitive payments. However, international wire transfers require more checks and verification, so often take much longer.

EFTs vs wire transfers - Security

They’re both a really secure way to transfer money, but you should be aware of potential scams nonetheless. Always make sure you know the identity of the person you’re sending money to, regardless of the type of transfer you’re doing. It’s easier to check all the details are correct before the transfer starts than it is to try and reverse it afterwards.

More generally, both EFTs and wire transfers are subject to stringent security checks to make sure your money is safe. There are a range of financial regulators that monitor the activity of financial institutions like the Federal Reserve Board, the Federal Deposit Insurance Corporation, and the Financial Conduct Authority, which help ensure all transactions are as secure as possible.

Data used for both wire transfers and EFTs is encrypted during transmission, which helps ensure only authorized parties can access your personal information while the transaction is taking place. Alongside this, a lot of banks use other security measures, like two-factor authentication, which ensures only the individual authorized to make the payment is able to initiate it.

Sending limits

You can usually send larger amounts of money at a time via wire transfer, with more limitations on the maximum amount that can be sent via other EFTs. This makes wire transfers more useful for larger transactions.

Cost

Generally, EFTs are more cost effective than wire transfers, as financial institutions will often charge a fee for bank wires. However, if you’d like to transfer money abroad, you might find it easier to arrange a transaction through a specialist money transfer provider.

What is an electronic funds transfer?

An Electronic Funds Transfer (EFT) is a financial transaction processed automatically through an electronic payment system. EFTs are entirely electronic, with no physical money or paper checks being processed.

How EFTs work

EFTs are processed electronically through either the Automated Clearing House (ACH), a payment terminal, or an ATM before reaching the recipient’s account. The speed of these transfers depends on the payment method, but is usually between one and three business days.

The Automated Clearing House

The Automated Clearing House is an electronic clearing network for processing EFTs in the United States. Transfers are processed and mailed to recipient banks in bulk, every business day at pre-defined intervals.

Types of EFTs

There are several types of EFT, including:

Debit card transactions

ACH transfers

Telephone bill-payment plans where periodic or recurring transfers are completed

Online banking

Electronic fund transfers overseas

What is a wire transfer?

A wire transfer is a specific type of EFT, designed to move money from one account to another electronically. Wire transfers require secure messaging systems, like Fedwire or the SWIFT payment system, that allow banks to communicate with each other and process individual payment requests.

How wire transfers work

A wire transfer is the electronic transfer of funds from one bank account to another. As wire transfers are a type of EFT, there’s no physical transfer of money or checks. The sender will provide instructions for the transfer, including the recipient’s name, bank, account number, and the amount of the transfer.

The sending financial institution sends a message to the recipient’s bank through a secure system like Fedwire or SWIFT, and the recipient’s bank makes a deposit from its own reserve funds to the recipient’s account. The financial institutions then settle the payment between themselves.

Making a domestic transfer in the US isn’t necessarily cheap, but making international wire transfers can be considerably more expensive. A cheaper way of wiring money could be a specialist money transfer provider.

EFT vs wire transfer: Which is right for me?

Both have their uses, so it really depends on the type of transfer you’re making and the most important factor to you.

Time

Cost

Amount

Purpose

The type of payment

Security

Remember, it’s a good idea to put your own safety measures in place, like regularly reviewing your bank statement for any unrecognized transactions, and reporting any potential issues or cases of fraud to your bank as soon as you spot them.

Check your provider is regulated

You should only ever use regulated providers to transfer money. If a provider is not regulated, it’s likely to be a scam.

Remember: We will only ever recommend regulated financial institutions.

Other options for transferring money

There are other options for transferring your money, including:

Mobile money transfers

Cash pickup

Check

Home deliveries

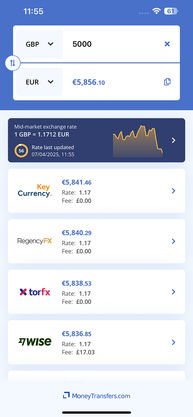

Best options for international money transfers

Wire and electronic transfers are valid choices for sending money abroad. However, their fees are too high, and the transfer speed is too slow. Instead, choose money transfer companies to get a better deal. Some offer a mixture of variable and fixed rate pricing. This means that you can get a good deal when sending small and large amounts of money.

TorFX is an example of a transfer provider that offers a better deal than bank transfers for sending money internationally. They do not charge fees for transfers but instead require a small markup percentage for currency conversions. Also, they offer multiple transfer methods to offer better flexibility for different customers.

FAQs

What’s the difference between a wire transfer and an electronic funds transfer?

How do you make a wire transfer?

Does Canada accept wire transfers?

Related Content

Related Content

Contributors

.jpg)