What Are the Safest Ways to Send Money Internationally?

Scams have become more and more common in recent years. According to the FTC, consumers lost nearly $8.8 billion to fraud in 2022. It’s vital that you find the safest ways to send money abroad so you don’t fall victim to scammers.

We’ve provided full details of what to look out for, warning signs of potential scams, and the safest ways to send money abroad. Whether you’re sending money home, helping friends and family, or paying for goods, find the safest way to make sure your money goes where it’s supposed to.

Search Now & Save On Your Transfer

The safest ways to send money internationally include bank transfers, reputable money transfer providers, and money orders. These methods offer high security with features like encryption, fraud prevention, and multi-factor authentication.

Credit cards add additional protection to your payments in case you don’t receive the product or service you’re expecting. Most transfer providers let you make payments by credit card. Some payment apps like PayPal also have buyer protection, making it easier to get your money back if you don’t receive what you’ve been promised.

Top three safest ways of transferring money

These are some of the safest ways you can make payments overseas.

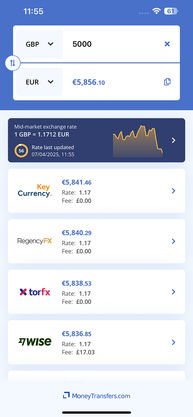

Wise

As a world-renowned bank, Wise is one of the safest ways you can make transfers. Their app includes multi-factor authentication, giving you the peace of mind that nobody can access your account without your knowledge.

While Wise’s fees are beaten by some providers, they offer the mid-market rate on foreign currency exchanges. This puts them ahead of the competitors that add high markups. They also let you pre-calculate your fees using their in-app calculator, making them more trustworthy overall.

Wise gives you access to a multi-currency bank account that can hold up to nine different currencies at once. Aside from our tests, Wise also regularly receives positive reviews on Trustpilot, Google Play, and the App Store. These reviews often highlight the app's ease of use, the transparent fee structure, and the efficiency of query resolutions.

Xe

With multi-factor authentication required to log in to the app, XE is a safe and secure way to send money overseas. They have a transfer corridor to over 200 countries worldwide, so are very likely to service your target destination.

XE charges no fees for transferring more than $500, making them one of the cheaper providers available. They process most payments in less than 24 hours, putting them in the faster bracket, and they have a high-value focus with a maximum transaction limit of $535,000 per transfer*

*Depending on the payment method you choose.

TorFx

As a highly respected provider of remittance, TorFX is a safe way to transfer money abroad. Founded in 2004, they’re one of the more established transfer providers on the market, which has helped them to build trust over time.

TorFX assigns you a dedicated account manager on signup. They can help you in all areas of your transfers, from finding the best deal to showing you how to navigate the TorFX app. This goes some way to explain why TorFX is rated so highly on review sites like Trustpilot, achieving a staggering 4.9 stars out of 5.

How to stay safe when sending money internationally

There are a few top tips you can follow to stay as safe as possible when sending money abroad. These apply no matter how you’re sending money.

Always use a regulated financial institution

Only send money to people you know and trust

Always check your recipient’s payment information

Protect your bank accounts and personal details

Be aware of payment scams

Check your provider is regulated

You should only ever use regulated providers to transfer money. If a provider is not regulated, it’s likely to be a scam.

Remember: We will only ever recommend regulated financial institutions.

The safest ways to send money

Because of the many options available when it comes to making money transfers, it can be difficult to know how safe they are. This list shows you the different ways you can safely make international money transfers.

Bank transfers

Sending money by bank transfer is one of the safest ways to transfer money internationally. This is because of the layers of security involved with making a bank transfer. If you make a bank transfer internationally, it’s likely you’ll be making a wire transfer. Wire transfers are expensive, but relatively fast when compared with domestic ACH transfers.

Banks use the secure Society for Worldwide Interbank Financial Telecommunication (SWIFT) network to communicate with each other when making transfers overseas. The network is only accessible to regulated banks connected to it, making any payments made in this way extra secure.

The instructions for your wire transfer are sent through the SWIFT network to the recipient’s bank, either directly, or through an intermediary bank. While using this network is expensive, and the costs of wire transfers reflect that, it is one of the most secure ways of transferring money internationally.

How to wire money safely

Top tips on how to keep your wire transfer as safe as possible.

Use a regulated provider

Protect your personal information

Never wire money to anybody you don’t know

Check your bank statements regularly

International money transfer providers

International money transfer providers use a different method when sending money overseas, but this is also very secure. Rather than relying on intermediary banks within the SWIFT network, transfer providers use pools of money held in different countries to make your transfer.

For example:

You’re based in the US and you transfer funds to someone in the UK using Wise

You pay for your transfer, which Wise will deposit into their US account

Wise will then collect money from their UK pool of money and send it to your UK-based recipient’s bank account

Money transfer providers keep your money safe through secure encryption technology and strong fraud prevention methods. Often, providers will publicize this specifically on their websites.

For example, Wise keeps the money you hold with them safe through country-specific deposit insurance schemes like the FDIC and FSCS. They also provide real-time notifications when you spend with your card, and have their own dedicated fraud team.

XE also references their state of the art security on their website, and access to services for anti-money laundering and fraud prevention.

P2P Payment apps

Peer-to-peer (P2P) payment apps are another secure money transfer method. Like transfer providers, they have layers of security to protect you and your money. However, because transactions with most apps can’t be reversed, they’re also popular targets for scammers.

Financial institutions may not legally have to refund you your money if you’ve been scammed while using a payment app, so it’s important to be careful.

How to send money with payment apps safely

Here are some of the key ways you can keep your money safe when using a P2P payment app.

Enable multi-factor authentication

Use buyer protection

Link a credit card to your app

Verify the person you’re transferring funds to

Money orders

Money orders are less stringently regulated than banks and money transfer providers, but there are still some security measures in place. Money orders are more secure for all parties than personal checks, as the payer’s address isn’t included on them.

Money orders are generally considered one of the safest ways to send a reasonably large amount of money through the US postal service, but they do have a cap at $1,000. If you need to send more money than this, it’s safer to use a bank or money transfer app.

As long as you have the receipt, you can track your money order after you’ve sent it. If anything goes wrong, your receipt allows you to recover any funds if the money order is lost, stolen, or damaged.

Scam alert

If you receive a money order for more than an item or service you’re providing, and the sender asks you to return the difference, stop. This is a scam. The money order is most likely to be fake, and you could risk sending a scammer money from your account.

How to send money orders safely

Follow these steps to stay safe when sending money orders.

Beware of unexpected requests

Avoid sending money orders to people you don’t know

Always use a money order provider

Keep your receipt

Checks

You can send checks with a greater degree of safety than cash, as they can only be deposited by the person named on the check. However, they’re not as safe as electronic transfers sent through money transfer apps, or money orders. As they’re often sent in the post, they can also get lost, but in cases like this, they are easily cancelable.

How to mail a check safely

Top tips to keep your check mailing safe.

Restrict the check

Send the check via certified mail

Drop the check at a secure postal location

Track your checks

Cash

Cash can be a convenient way to send money, but it’s one of the least secure ways of transferring money overseas. When cash is the only option, you can arrange its transfer securely by using money transfer services that offer cash deposits.

Providers like Western Union allow you to deposit cash at one of their locations. They will then send the equivalent amount (minus any fees) to a designated pickup location where your recipient can collect it. Some providers even offer cash delivery services, and will deliver cash directly to your recipient’s address. Remitly and MoneyGram offer cash delivery services.

Never send cash in the post

You should never send cash in the post as it may get lost or stolen, including gifts in birthday and Christmas cards. There are lots of ways to safely send cash abroad using a money transfer service.

How to send cash safely

There are ways you can send cash safely.

Always use a registered transfer provider

Avoid sending cash to people you don’t know

The safest way to send money through the mail

The safest way to send money through the mail is via a money order. Use a specialist money order company to send money through the mail, rather than cash or a check. Money orders contain less personal information than checks, and can only be deposited by the named recipient. You should never send cash in the post as it can easily get lost or stolen.

Common money transfer scams to be aware of

These are some of the most common scams you should be aware of before making international transfers.

Online payment scams

Online shopping scams

Tech support scams

Real estate wire scams

Online payment scams

Online payment scams attempt to get you to make an online payment for a service you will never receive. A common online payment scam involves a scammer contacting you claiming a payment you tried to make has not gone through. They will tell you that to fix the problem, you need to authorize a payment to a ‘test’ account. This account will belong to the scammers.

Avoid this scam by always contacting your payment app’s customer service department directly using their official website if you receive any calls from them.

Online shopping scams

Scammers may pretend to be legitimate sellers on sites like eBay and the Facebook marketplace. In an online shopping scam, you’ll be encouraged to pay for an item or service which you’ll never receive.

Avoid online shopping scams by checking the reviews of sellers on the shopping website, and only making a payment via the website’s official checkout system. Never use a bank transfer or online money transfer to pay for goods or services online.

Refund scams

In refund scams, scammers will contact you by email to state a transaction has been approved in your name. This is usually an Amazon transaction, but may also be through other large payment sites like eBay or the Google Play store, or subscription services like Netflix.

The email will include a telephone number for you to call to get your refund. This will put you through to the scammers, who will ask you to download software that gives them access to your computer, like AnyDesk or TeamViewer. They will then tell you they’re going to refund the amount back to your bank account. They will usually ask you to type this in yourself.

The scam will then make it look like too much money has been paid into your bank account, usually by a thousand dollars or more. They will then ask you to ‘return’ this amount to their own bank account by purchasing gift cards or arranging a cash deposit of the same amount.

Do not send any money. Hang up the phone and contact your bank immediately. They will be able to confirm if anything has been paid into your account.

If you receive a suspicious email discussing a transaction you do not remember making, report the email as a phishing attempt. You may see a phone number on the email. Do not call this number. It will put you through to the scammers. If you’re concerned about activity on your account, contact the customer service team via the details on their official website.

Real estate wire scams

It’s important to be aware of real estate wire transfer scams. If you’re in the process of buying a house, you may be vulnerable to real estate wire scams. Scammers may pretend to be the owner, real estate agent, or closing attorney for the property you’re looking to purchase. They will then proceed to send you instructions for how to wire money to their account.

Never send a wire transfer under these circumstances. Always contact your agents via their official contact details to verify any account information.

What to do if you’ve been scammed

If you think you have been tricked into transferring money to a fraudster, there are two things you should do.

Contact your provider

Report the incident to the Federal Trade Commission (FTC)

Notice: What’s the safest way to receive money?

If you need to receive money from a buyer, you should be careful how you accept payment. The safest way is to receive a payment via an app like PayPal or Cash App. With apps like these, you only need to share an email address to receive money. You can also arrange payment via credit card.

It’s riskier to request a bank transfer, as this involves sharing your details with a stranger.

Popular countries to transfer money to

Check out our country list below for a summary of the safest ways to send money to them.

How to safely transfer money to someone without a bank account

Sending money to someone without a bank account can be tricky, as your payment methods are much more limited. But, there are plenty of ways to stay safe when sending money to someone without a bank account. Here are some of the top methods.

Prepaid debit cards

Prepaid debit cards allow users to load money onto a card rather than using bank accounts. They’re available from some companies online, or in person from stores like Walmart. You can top up your recipient’s prepaid debit card online, but you’ll usually need to pay a loading fee.

You can add money to someone’s prepaid debit card securely via the card issuer’s website, or in store at certain locations. This is a secure method of payment as the money goes directly to the recipient’s card.

Prepaid gift cards

Most prepaid gift cards are linked to a particular store or brand. This gives them less spending versatility than prepaid debit cards, but they usually come with minimal fees. They can usually only be used until the initial funds have run out, and cannot often be topped up.

Gift cards are useful if you know the recipient well, as you can send them a gift card for a store they particularly like or use often. Prepaid gift cards are secure in that they can only be used until the balance on the card has been spent, and only at certain stores.

Try to order the gift card for delivery

Try to order the gift card for delivery on the company’s website. This adds additional protection and helps prevent the card being lost or stolen in the post.

Money transfer agents

Money transfer agents are people or companies that can facilitate a transfer on behalf of a money transfer operator. They can arrange cash deposits to specific collection points on your behalf, to make sure your transfers are kept safe.

Extra security measures are usually put in place for these transfers, like needing the recipient to confirm a prearranged PIN, or asking to see their ID at the collection point.

Stay safe when sending money - use a trusted transfer service

The safest ways to send money are through banks and money transfer services. You should always make sure your chosen provider is fully regulated before making an international transfer. If you follow basic precautions, you can keep yourself and your money as safe as possible when you’re transferring funds overseas.

FAQs

If I send money to someone, can they see my bank details?

How do I send money discreetly?

Can someone scam you if you give them your Cash App details?

Is it ever safe to send money to a stranger?

What’s the safest way for international students to transfer funds?

Related Content

Contributors

.jpg)