Paysend is a global financial technology company that allows users to make cross-border card-to-card transfers, as well as payments to bank accounts and digital wallets. In an increasingly interconnected world, the demand for cheap money transfer services continues to rise, and Paysend is dedicated to catering to this market. In this review we will take a closer look at the intricacies of this money transfer operator; from exchange rates and transfer fees, to location coverage and customer feedback.

About Paysend

Founded in April 2017 by a team of experts from the financial services field, Paysend identifies as “a global FinTech company on a mission to change how money is moved around the world.” By developing a faster, more straightforward money transfer system, Paysend has acquired more than 4 million customers and 17,000 small-to-medium sized enterprises, located around the world

Through card-to-card transfers - Paysend connects 12 billion card users globally - customers have access to a convenient and low-cost way of transferring money across borders. This review aims to clear up any confusion about this money transfer company, ensuring our readers gain a fuller understanding of how Paysend works, how much it costs, where it can be accessed and by who.

Paysend Exchange Rates, Fees and Costs

Much like other international money transfer companies, Paysend charges transaction fees to cover administration costs and generate a profit. Below is an overview of the fees that Paysend charges, as well as the exchange rates offered.

Exchange Rates

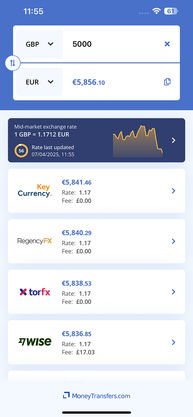

Paysend applies a 0% exchange rate margin: one of the most attractive parts of the service. The company has direct connections to currency exchanges in more than 100 countries, and can therefore facilitate foreign currency transfers that use the real-time mid-market rate. Total transparency is guaranteed throughout the process, with the displayed exchange rate remaining locked in for the duration of the transfer.

Transfer Fees

The Paysend transfer widget displays the exact amount to be paid in fees, without any hidden costs appearing later on. These costs are consolidated into a flat-fee, irrespective of the amount being transferred, with a list of tariffs for the different currency routes can be found on the company website.

For instance, customers sending money from Europe are charged €1.50 EUR, while those sending money from the United States, Canada, or the United Kingdom will pay $2.00 USD, $3.00 CAD, and £1.00 GBP respectively. These fees are charged to the sender when transferring the funds.

Additional Costs

One of the biggest advantages and integral aspects of this operator’s business model, is the total transparency guaranteed by Paysend, which rules out any chance of being issued unexpected or hidden fees. When making your transfer, Paysend presents the exact amount due to be withdrawn from your bank, as well as the fees that will be charged, the exchange rate your funds will be converted at and the amount the recipient will get.

Paysend eliminates intermediaries by working directly with international payment systems such as UnionPay, Mastercard, Visa and other leading providers..

It is important to note, however, that your bank may charge you additional processing fees when paying for your transfer. The recipient may also incur other charges such as landing fees and intermediary fees which Paysend has no control over.

In case you see unexpected charges on your card statement, you should get in touch with your bank’s customer support team for clarification.

Top Destinations for Sending Money With Paysend

As a trusted remittance platform with global reach in the money transfers space, Paysend is able to assist customers based in 49 countries send international transfers.

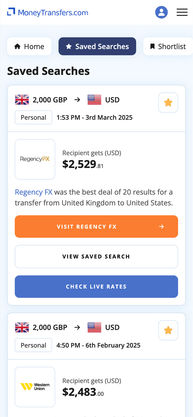

There are 100 different sending countries to choose from, and no two currency routes experience the same level of traffic. Certain transfer corridors are busier than others and although the provider does not explicitly state what the top corridors are, it has quoted the World Bank in affirming the following as the top currency routes for people sending money from the UK:

Customers sending money to India with Paysend can choose to transfer money directly onto Mastercard, into bank accounts or through UPI. Money is usually transferred on the same day.

Customers using Paysend to transfer money to Nigeria can make payments directly to Access Bank accounts, MasterCard cards, cash pick up or through SWIFT.

Customers can use Paysend to transfer money online to MasterCard cards or bank accounts in France. Money is usually transferred on the same day.

Pros and Cons of Using Paysend

Paysend is a simple and innovative platform and in this section we will provide a summary of the leading pros and cons of using the operator to send money internationally:

Pros

Cons

What Type of Transfers Can You Make With Paysend?

Paysend supports the following three types of international transfers:

Card-to-card Transfers: Funds are sent directly to the recipient’s card based on the information provided by the sender. Once the funds have been deposited, the recipient can choose whether to withdraw from an ATM or use for card payments

Bank Deposits: This payout option was introduced in February 2019 and allows senders to transfer funds from their cards directly to the recipient’s bank account. It is convenient, safe and fast for both B2B and P2P payments

PaysendLink: Using the recipient’s phone number, the sender can transfer money via PaysendLink. The recipient will be notified of the incoming transfer and given the option to direct it to their cards, bank accounts, or withdraw the funds from an ATM

In addition to the above transfer types, Paysend imposes transfer limits. Customers can send funds up to a maximum of $1,000, £1,000 or €800, every six months.

These limits can be increased incrementally by providing additional verification of your identity as per the following requirements:

Up to £5,000

You will be required to confirm your personal details by providing any one of the following:

Current signed passport

National identity card bearing your photograph

Driving license

Up to £10,000

To increase your transfer limit to £10,000 you will also need to include proof of address, which can include any of the following documents:

Utility bill issued within the last 3 months

Local authority council tax bill for the current tax year

Bank, building society or credit card statement or passbook dated not older than three months which is verified through being stamped, signed, or otherwise marked by the issuing organisation

Driving license if not already used as your proof of identity

Tenancy agreement for the current year

Over £10,000

To increase your transfer limit above £10,000 you will need to declare the source of your funds. Any of the following documents will be accepted:

A certified bank statement not older than 3 months; must not have been used as proof of address

Employer payslips for the last 3 months, accompanied by a bank statement

If the funds are coming from a pension scheme, supporting HMRC documents are accepted

If the source of funds is a loan, you will be required to provide a letter from a solicitor to support the bank statement

How Long Will It Take to Receive Money Using Paysend?

According to the provider, payments are processed instantly and money delivered within minutes. However, some transfers may take up to 3 business days to be delivered, depending on the receiving country and bank. It is also worth bearing in mind that some transfers may be subject to additional checks in the receiving country, potentially causing further delays.

What Payment Methods Can I Use When Sending Money With Paysend?

How you pay for your transfer and how the beneficiary receives the funds are two fundamental aspects of any money transfer process. There is a need to balance convenience, speed, and low costs to get the best deal. Currently, the company only accepts card payments: you can link a Mastercard or Visa debit, credit or prepaid card to your account which can be used to pay for your transfer. Funds become available faster when card payment is used therefore speeding up the transfer process.

What Are the Best Reasons to Use Paysend?

There are a number of reasons to use Paysend, the first being the competitive fixed fee applied to international transfers. Although other providers advertise free money transfers, these deals often come with unique terms and conditions, but the Paysend fee structure is transparent and straightforward. A low-cost flat-fee is applied to all international money transfers, the cost of which is clearly displayed from start to finish via the Paysend widget.

Another reason to use this company is their commitment to matching the mid-market rate. Zero markups are applied to foreign currency transfers which is hugely beneficial, especially to customers transferring large amounts of money abroad. A third and final reason to use Paysend is the high security standards upheld by the company. This operator deals directly with major card issuers - Visa, Mastercard, UnionPay etc. - and customer data is protected by the highest PCI DSS standard with integrated fraud prevention systems. Find out more about the regulatory compliance and security protocols in the next section.

Can I Trust Paysend?

This is one of the most important questions when it comes to using a money transfer service, and Paysend has earned itself a reputation for trustworthiness in the industry. In this section we will provide a list of reasons to trust the security of Paysend services:

Regulatory Compliance

The company is registered and regulated by a number of financial bodies. Paysend Plc is an authorised electronic money institution solely focused on facilitating international money transfers for businesses and individuals.

In the United Kingdom, where it is headquartered, the provider is authorised and regulated by the Financial Conduct Authority (FCA) under reference number 900004. This license permits the company to carry out a number of activities, including:

Depositing cash to a receiving account

Withdrawing funds from a payment account

Issuing payment instruments

Remitting money

In December 2019, Paysend received a money service business (MSB) license to conduct business in Canada.

Key Industry Partnerships

Paysend is a registered ‘Visa Direct’ and ‘MasterCard MoneySend’ originating institution. These partnerships mean the provider benefits from superior payment and cross border money transfer technologies, extending these services to their user base.

Encryption and Customer Data

When it comes to protecting customer data, transactions captured on Paysend are safeguarded under the PCI DSS Level 1 standard.

Thanks to its innovations within the money transfers sector, Paysend has attracted significant investor interest from the following companies:

GVA Capital

Plug and Play

MARCorp Financial

Digital Space Ventures

To add to these existing security layers, Paysend also safeguards card transactions with 3D Secure encryption: an XML-based protocol. Furthermore, all the access points and ports to the Paysend website are encrypted using enterprise-grade SSL.

Investors and Awards

As it stands, Paysend has secured over $157.6 million in funding and employs around 163 professionals in its fintech operation. The company has also featured prominently in authoritative industry websites such as:

Finextra

Yahoo! Finance – A brand owned by Verizon Media

The Courier- A domain owned by DC Thomson & Company Limited

In addition to this, Paysend has been rewarded for its innovation and exemplary money transfer services by receiving multiple industry awards, including:

PayTech 2018 Awards – Best Consumer Payments 2018

FinovateSpring 2018 – Leading FinTech product 2019

Mastercard – Top tier (5%) for processing quality

It is worth noting among all of these positives that Paysend does not currently participate in any deposit guarantee scheme. This means that customer funds held in virtual wallets are not protected by the Financial Services Compensation Scheme and do not earn interest.

Does Paysend Have a Mobile App?

Enjoy the convenience of sending money on the go with the free Paysend mobile app, available on the App Store and Google Play Store.

On the Google Play Store, the Paysend app has a rating of 4.0 out of 5 stars, with more than 93,500 user reviews. The iOS version of the mobile app also has a score of 4.7 out of 5 with more than 2,200 ratings.

In addition to sending money transfers, user can also use the app to do the following:

Sign up for an account

Add and amend recipients

Check the status of your transfers

View history of all transactions

Check exchange rates and transfer fees

What Do Users Have to Say About Paysend?

Looking at online feedback posted on consumer review site Trustpilot, Paysend users appear to have a very positive view of the company. More than 29,700 user reviews have been posted on Trustpilot, with 92% of these awarding the company 4 or 5 stars. We have picked out recurring comments to see what customers are saying about Paysend services:

Pros

Cons

Paysend customer service representatives appear to take the time to respond to all feedback posted on Trustpilot, which attributes to their reputation as an attentive and supportive service provider.

How to Get Started With Paysend to Send and Receive Money

We want to assist those of our users who have not yet used this service to send or receive money, by providing clear and concise step-by-step instructions.

Sending Money Online With Paysend

Paysend allows you to send money online to over 150 countries for just £1. It’s fast and hassle free and once you get started, you should be able to send transfers in just a few minutes. We’ve broken the process down into 4 easy to follow steps:

Sign Up

Enter the Sending Amount

Provide the Payment Details

Submit the Transfer Request and Confirm all Details

Sending Money Through the Paysend Mobile App

The Paysend mobile app is a fantastic and hassle-free way to send money on the go. It works in a similar way to the website and should only take a few seconds for you to send your first transfer. Simply follow our four simple steps to get started:

Download the Paysend Mobile App

Enter the Amount You'd Like to Send

Enter the Recipient's Details

Send the Payment

Receiving Money From Paysend to Your Bank Account or Debit Card

In most cases, Paysend will send money directly into a bank account or onto a debit card and there is very little for payees to do. In most cases you’ll receive your online money transfer instantly, although in some circumstances money transfers can take up to 3 business days to arrive. Follow these two steps to receive your funds:

Inform the Person Making the Transfer of Your Bank Details

Receive Funds

Receiving Money From Paysend to a Cash Pick Up Location

In certain countries, such as Nigeria and the Philippines, Paysend allows users to send cash to a pick-up location within that country. This can be particularly helpful to recipients that don’t have bank accounts and as most transfers are instant, it is fairly hassle free. To receive money from a cash pick up location just follow these simple steps:

Request for the Reference Number and OTP

Bring a Government Issued ID and Go to the Chosen Location

Receive Funds

Receiving Money From Paysend to a Mobile Wallet

Bangladesh and Zimbabwe are just two of the many countries that allow Paysend users to make transfers directly into digital wallets using Paysend link. The process is straightforward, and you should receive your funds immediately, although money transfers can sometimes take up to three business days. To get started follow these simple steps:

Inform the Person Making the Transfer of Your Mobile Phone Number

Receive Notification About the Incoming Transfer

Other Money Transfer Providers

FAQs

How to cancel your Paysend transfer?

What customer support options are available?

Can I send anonymous payments on Paysend?

Is Paysend Russian?

Can I send money from Paypal to Paysend?

Paysend user feedback

Comments

Fredrick Ndongwe

Difficult to register and use

Anonymous

Too expensive

Anonymous

Flaw in program and help was decidedly unhelpful

Anonymous

It has a lot of fault especially when it comes to payment

Anonymous

Asked for too much personal information